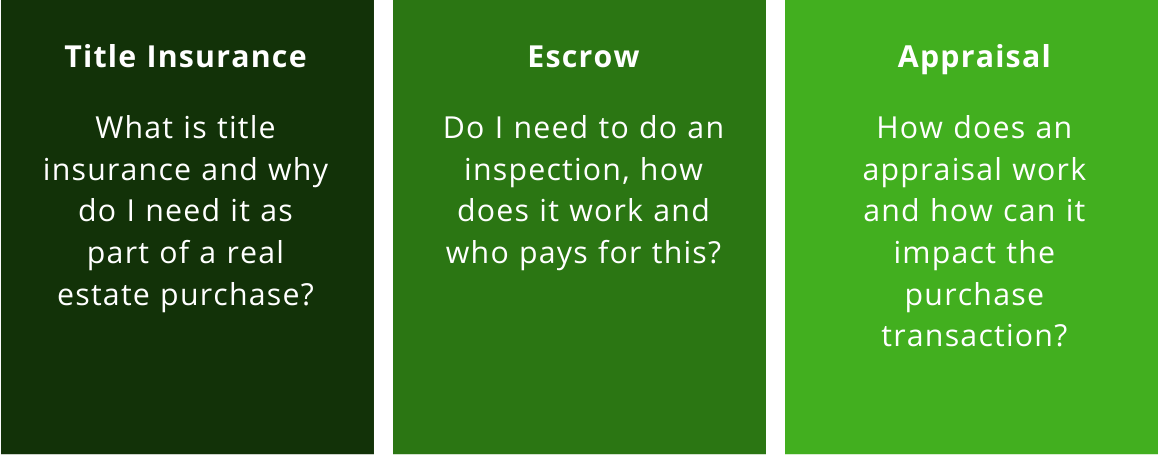

What is Title Insurance?

What is Title Insurance?

First, the word “Title” is a collective term for all of your legal rights to own, use and dispose of land. Title includes all previous ownership, uses and transfers. To legally transfer real estate property, a title search must be performed, and, in most cases, the title must be found free of any circumstances that could endanger your right of ownership. Title insurance protect against the possibility of future loss should your legal rights to your property be challenged.

For a one-time premium paid during the closing process, your title insurer assumes responsibility for all legal expenses to defend the title to your property if ever challenged. If the defense is unsuccessful, you are reimbursed for any reduction in the value of the land. It is an important layer of security.

There are two types of Title Insurance: A lender’s policy and an owner’s policy. The lender’s policy protects the lender’s interest in the property for the amount of the mortgage loan. An owner’s policy protects the homebuyer for the full property value.

What Does An Owner’s Policy Cover?

An owner’s policy protects your interest in the property against such hidden hazards as:

What Is A Title Search?

A title search is a detailed examination of all available public records on a property to verify the seller’s right to transfer ownership, and to discover any potential challenges in the closing and ownership process. A title search should reveal unpaid taxes, unsatisfied mortgages, judgments against the seller, and restrictions limiting the use of the land. However, even the most diligent search may fail to reveal some hidden hazards, such as those mentioned above that Title Insurance protects from.

How Long Does Title Insurance Coverage Last?

A lender’s policy lasts until the mortgage is paid in full. An owner’s policy remains in force as long as you or your heirs have an interest in the property. If challenges to title arise after the property has passed to your heirs, the title insurance company would defend the title for them just as it would for you.

What Is Escrow & How Does It Work?

As a buyer or seller, you want to be certain all conditions of your sale have been met prior to property and money changing hands. The technical definition of an escrow is “a transaction where one party engages in the sale, transfer, or lease of real or personal property with another person who delivers a written instrument, money or other items of value to a neutral third person, called an escrow agent”. The escrow agent holds the money or items for disbursement upon the performance of a specified condition.

Your role on closing day

At closing, your participation will involve a couple of steps:

Sign legal documents

This falls into two categories: the agreement between you and your lender regarding the terms and conditions of the mortgage, and the agreement between you and the seller transferring ownership of the property. Be sure to read all documents carefully before signing them, and do not sign forms with blank lines or spaces.

Pay closing costs and escrow items

There are numerous fees associated with getting a mortgage and transferring property ownership. Usually, the borrower pays these fees with a check at closing. Some fees can be added to the loan balance, or the borrower can pay a higher interest rate and have the lender pay the fees.

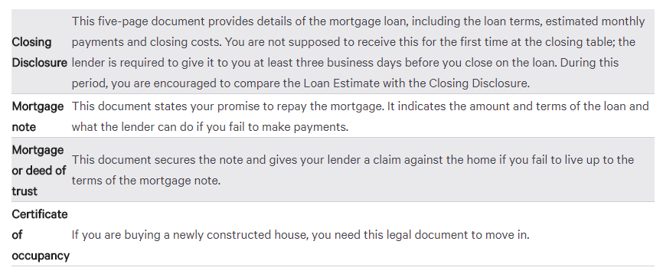

Closing documents

You will receive the following important documents: